India enters 2019 on the cusp of a digital revolution, mainly due to major influencers. First, we have a regulator defining the landscape by innovation-led policies, fuelling new-age business models and maintaining security and risk management standards to highest levels.

Second, we have a government that is focused on moving towards a digital or less-cash economy. Third, we have banks embracing technology to accelerate digital payments, proliferation of financial inclusion and superior customer services. And last, we have fintech innovators who are re-imagining solutions for our day-to-day problems and providing superior consumer experience for digital payments.

The Unified Payments Interface (UPI), the most advanced payment system in the world, was launched in 2016, designed on the principles of interoperability, consumer choice and forging partnerships between banks and fintechs, leveraging each other’s strengths.

The RBI’s payment system division DPSS, under the governorship of Raghuram Rajan, played a key role in bringing banks together to promote this initiative. Support of the Indian Banks’ Association (IBA) and leading lenders has been a critical factor in its success.

In the second half of 2018, the National Payments Corporation of India (NPCI) launched UPI 2.0 with the support of regulatory teams under former RBI governor Urjit Patel and deputy governor B P Kanungo to incorporate path-breaking features.

Several milestones were achieved in domestic payments last year. India’s RuPay Card crossed 500 million and Bharat BillPay on-boarded over 100 billers in its ecosystem. The Aadhaar payments services, too, surpassed 100 million unique customers every month.

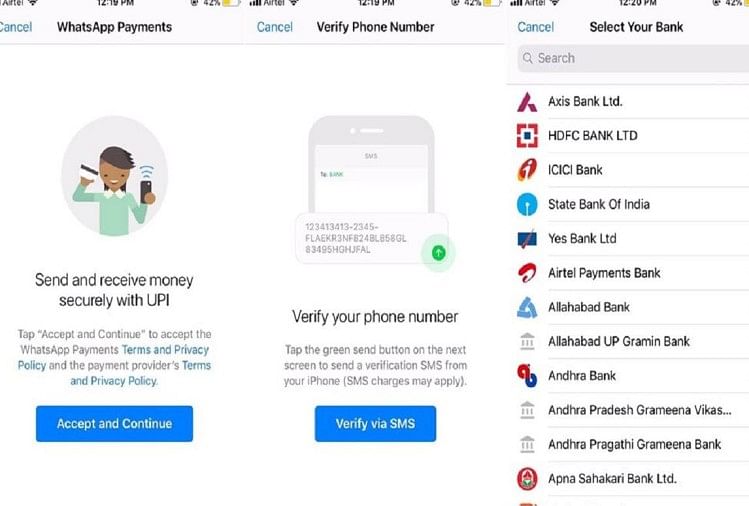

After demonetisation, the UPI-based ‘Bharat Interface for Money’ (BHIM) app, launched by Prime Minister Narendra Modi, has acted as a catalyst to nudge many third-party providers to launch the UPI app. We are now seeing the results. Sticking to the design principle of “consumer choice”, there are now over 90 BHIM UPI apps provided by banks or third party providers to customers of 130 banks.

The Supreme Court’s decision to limit the use of Aadhaar database was a setback. The fintech community is relying on the government to identify a solution to use Aadhaar systems based on voluntary sharing by the customer. The NPCI had to stop the e-NACH (National Automated Clearing House) using e-sign due to the SC judgment. However, we are working to create alternatives, but it may take time.

While it was a practice to look towards the latest trends in Silicon Valley in the US, with UPI, the West has turned to partner with India for innovation. Many global giants (Google, WhatsApp, Amazon, Samsung, Truecaller, Xiaomi, etc) and Indian unicorns (Paytm, PhonePe, Hike, etc) have joined the UPI bandwagon in collaboration with banks.

Unlike China that operates mobile payments mostly under two players in a closed loop manner, the RBI has been clear from the start to set UPI as an interoperable system. When it comes to mobile payments and financial inclusion using Aadhaar, India has an edge due to innovation.

While there are multiple ways for making payments, the market is broadly divided into three parts — a) financial inclusion that covers the JAM trinity, i.e. JanDhan, Aadhaar and mobile (additionally, it covers Direct Benefit Transfers, e-KYC, etc), b) mobile and internet payments powered by UPI, IMPS (Immediate Payment Service), net/mobile banking and interoperable QR codes, and c) card-based payments.

In the coming years, we will see a significant shift to a mobile-first strategy with consumers using functionality rich and user-friendly apps for P2P (peer-to-peer) or P2M (peer-to-merchant) payments. The electronification of all kinds of C2G (citizen-to-government) payments is a big opportunity. I’m glad to see the efforts from all government divisions pushed by the ministry of electronics and information technology (MeitY) and the department of financial services (DFS).

If the growth momentum continues, we hope that the use of UPI will take the shape of citizen-scale payments system. Volumes may come down in the short term once firms go slow on promotional offers. However, the outlook is very strong for medium to long term.

We have started an awareness campaign to protect customers from social frauds. But, more needs to be done. Now that diverse payment platforms are available to customers, our goal would be to drive adoption among the masses.

We have the potential and capability to do what China has done to build its digital economy, better and faster. Startups/fintechs, in collaboration with banks, should build specific-use cases to drive adoption that will be the main attraction of 2019.